Working Papers

Latent Human Capital and the Immigrant Mobility Advantage: A General Equilibrium Analysis

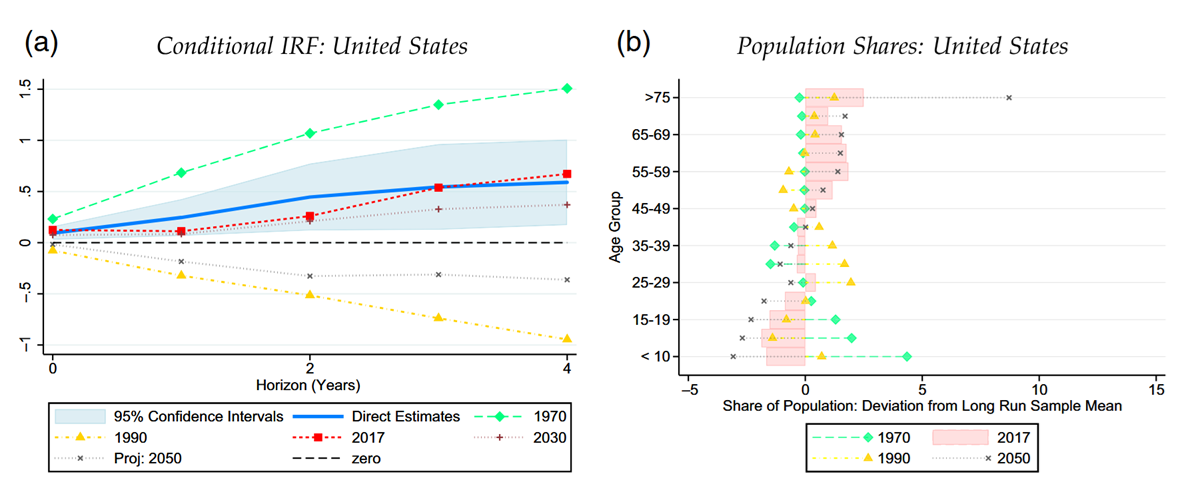

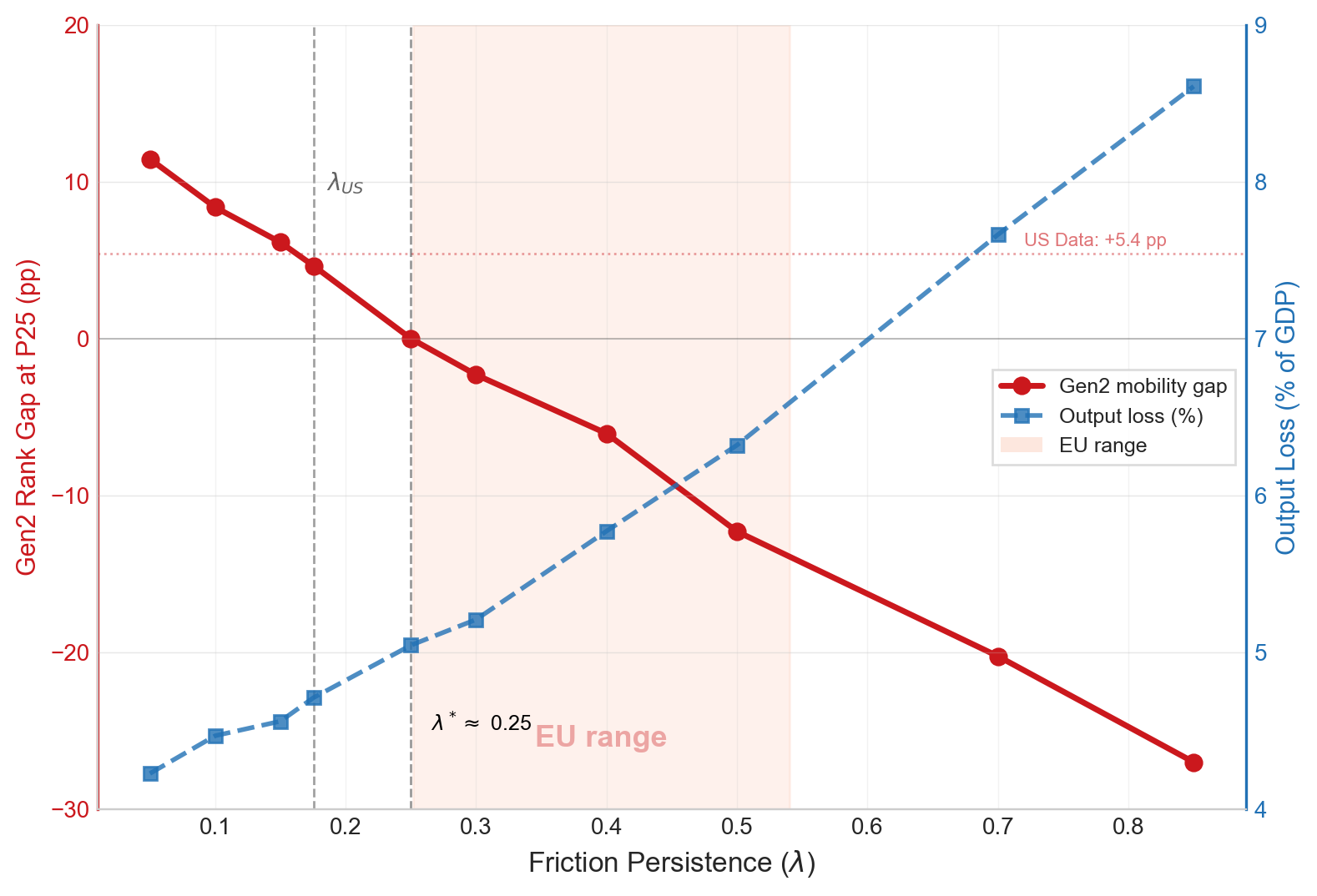

Children of low-income immigrants in the United States systematically out-earn children of comparable natives. I develop a dynastic general-equilibrium model to explain this "immigrant mobility advantage" and quantify the macroeconomic costs of the institutional frictions underlying it. The central mechanism is a wedge between latent human capital and realized earnings: immigrants are positively selected on ability but face institutional frictions that decay at rate λ. Calibrated to U.S. data, the model fits key empirical patterns and reveals that immigrant frictions cost the U.S. economy 4.94% of GDP. This loss is split between a static labor-misallocation loss (1.57 pp) and dynamic effects on intergenerational investment in human and physical capital (3.37 pp). I find that friction decay (assimilation) accounts for 87% of the second-generation advantage, with positive selection contributing the remainder. Finally, the model identifies a "sign-flip" threshold at λ ≈ 0.25, beyond which frictions persist too strongly for the mobility advantage to appear. Calibrating λ across ten OECD destinations recovers a distribution of friction values that straddles this threshold, consistent with the heterogeneous mobility gaps documented in the empirical literature.

The Comparative Advantage of Age

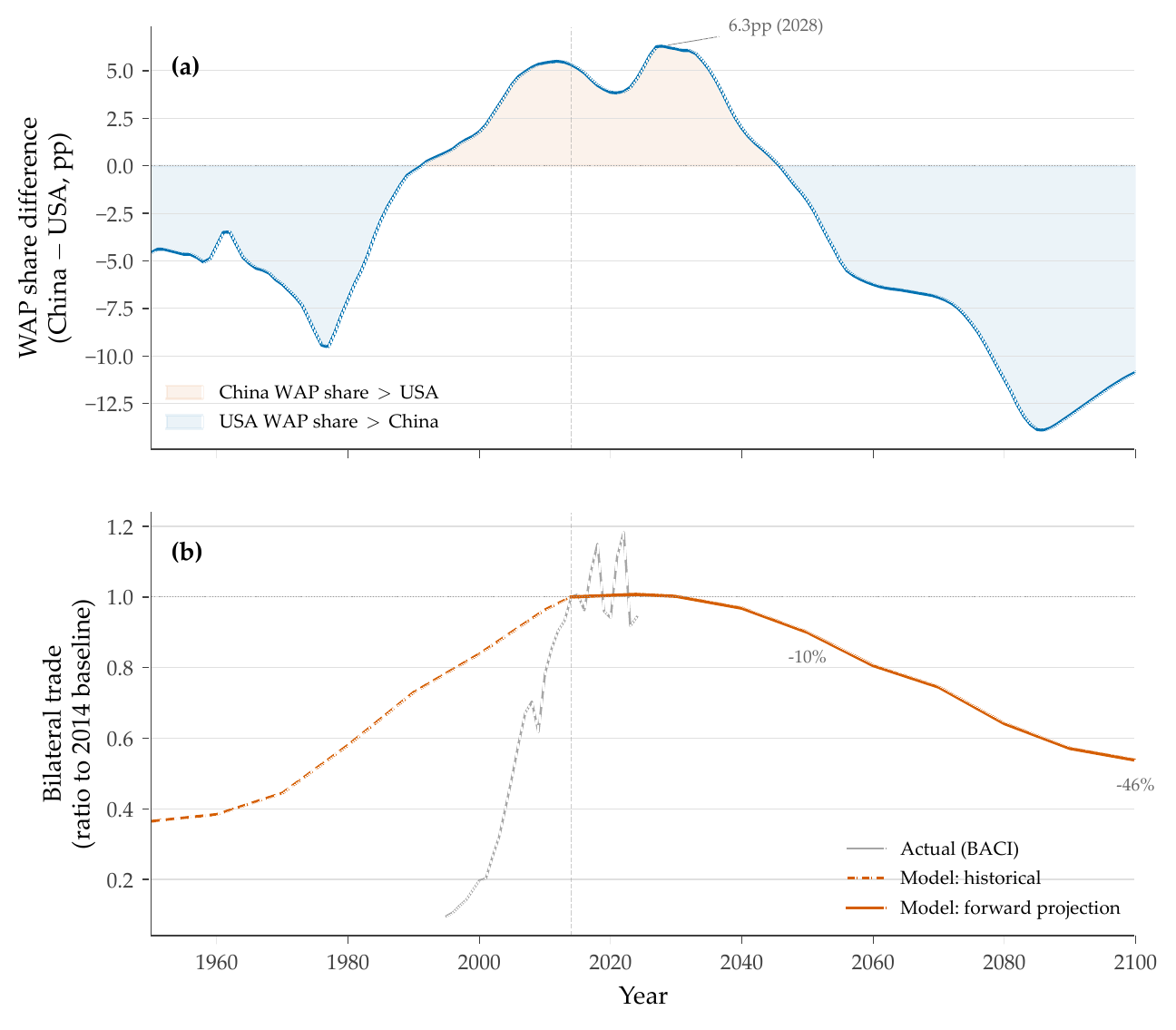

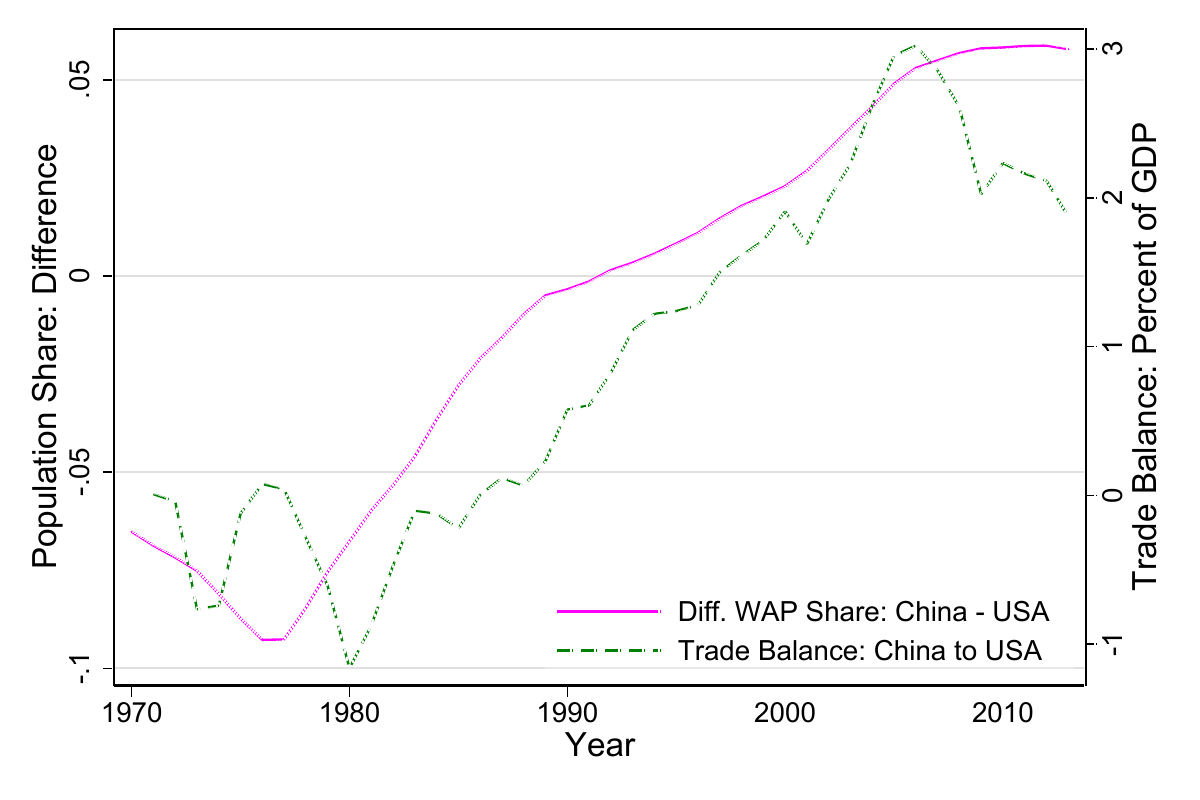

I develop a quantitative multi-country, multi-sector trade model in which population age structure shapes comparative advantage through age-dependent skills. Workers of different ages supply heterogeneous bundles of cognitive and physical abilities that appreciate or depreciate over the life cycle, and sectors use these skills with differing intensities. I embed this mechanism into a Ricardian trade model calibrated to 30 countries and 20 manufacturing sectors. Reduced-form evidence from a panel of 204 countries (1995-2024) documents a "grey advantage": a country's share of older workers is associated with a shift in its export mix toward appreciating-skill-intensive sectors. Evaluated in partial equilibrium, the calibrated model recovers 84% of this empirical relationship. General equilibrium adjustment then compresses the trade-composition response by a factor of ten, as endogenous wage and price changes absorb the sectoral reallocation but generate welfare-relevant real-income effects. Forward projections decompose the total demographic effect into a workforce-size channel (shrinking populations produce less) and a skill-composition channel (aging shifts the mix of skills, altering sectoral comparative advantage). The composition channel generates welfare effects ranging from −0.9% to +0.05%, comparable to standard trade-policy shocks, and exhibits a striking temporal pattern: historical demographic divergence supported positive composition gains, but as countries' age structures converge toward a common older profile, these gains are reversing. Bilateral trade flows reallocate accordingly, with the model projecting that China-US trade will fall by 10% and India-US trade will rise by 34% in the coming decades.

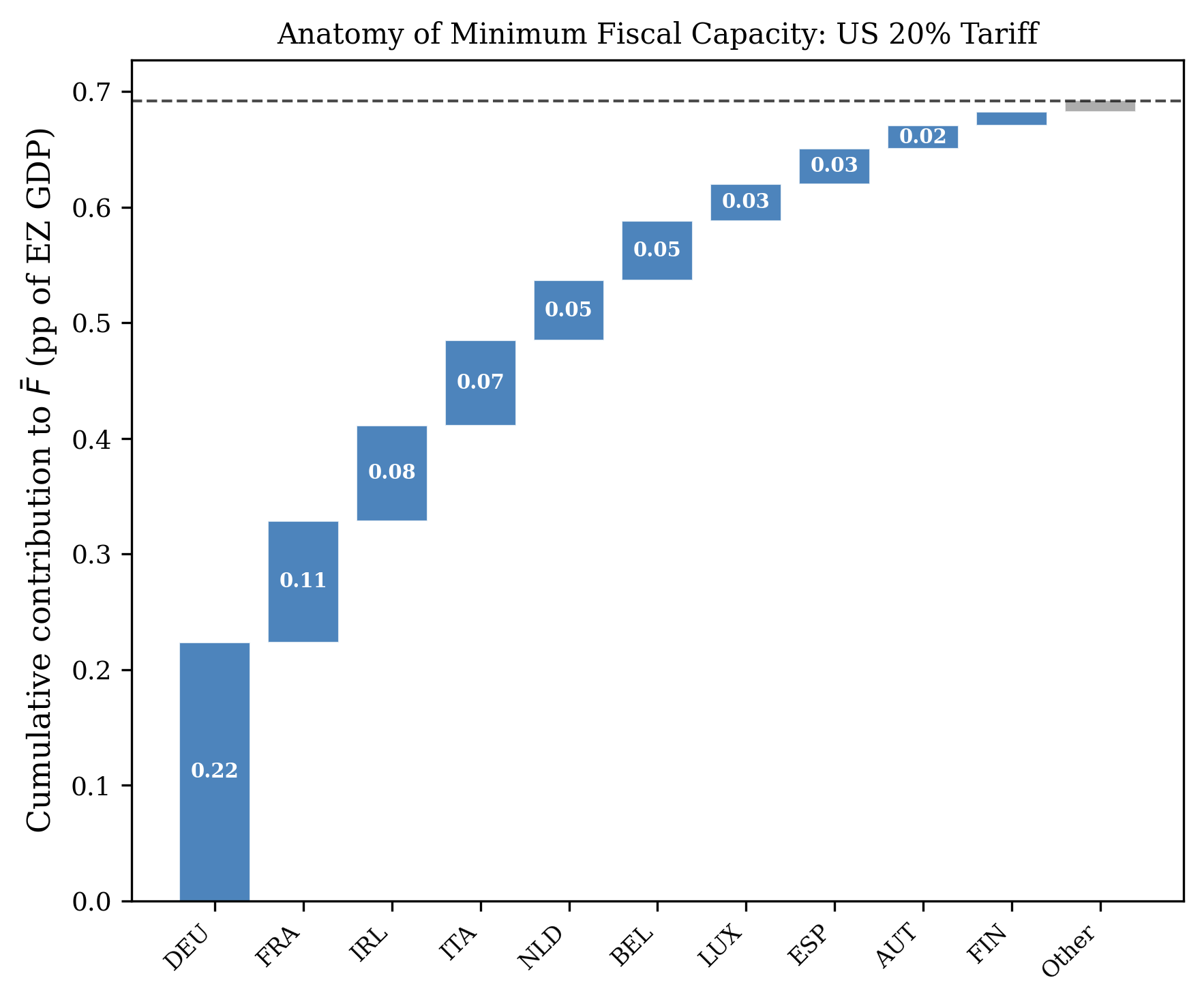

E Pluribus Euro: Minimum Fiscal Capacity for Collective Trade Policy in a Currency Union

As major powers deploy trade policy as coercion, what fiscal capacity does a currency union need to sustain a credible collective response? External trade shocks hit Eurozone members asymmetrically. Without fiscal transfers to pool costs, individual members face political pressure to seek bilateral accommodation with coercing powers, undermining the EU's collective bargaining position. I define a minimum fiscal capacity: the GDP-weighted transfer budget needed to make collective trade policy incentive-compatible for all members. In a quantitative trade model calibrated to the Eurozone, a 20% US tariff with EU retaliation requires a facility of 0.69% of Eurozone GDP (€97 billion). Existing EU institutions (cross-conditionality of fiscal transfers and qualified majority voting) reduce the practical requirement to 0.18% (€26 billion). Single market deepening generates large welfare gains but barely changes the fiscal requirement: integration and fiscal capacity are complements, not substitutes.

Explore the interactive visualization →

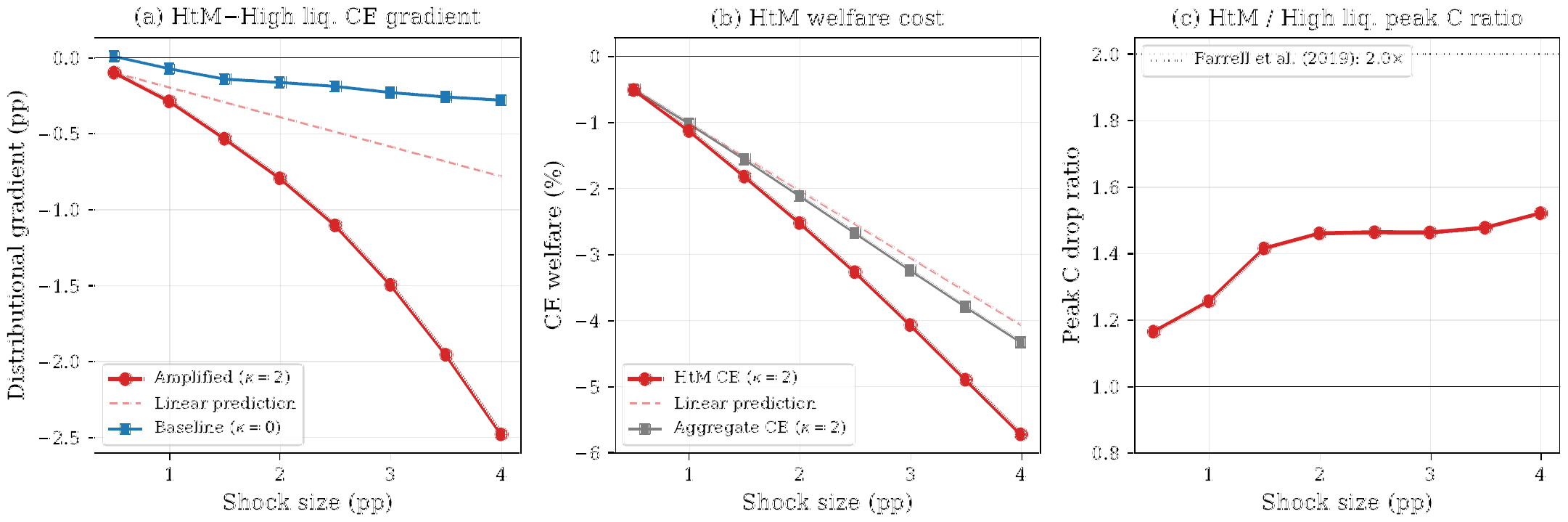

HANKs fr th Mmrs (Even If They Weren't So Great): The Distributional Cost of Recessions in a Heterogeneous Agent New Keynesian Model with Search Frictions and Human Capital

I build a two-asset Heterogeneous Agent New Keynesian model with search-and-matching unemployment and endogenous human capital dynamics to study who bears the cost of recessions. Human capital depreciates during unemployment, and workers with low human capital face both lower re-employment rates and lower re-employment wages, generating a self-reinforcing scarring trap. When human capital depreciation intensifies during severe downturns, this produces persistence and a sharp distributional divide. In a Great Recession-calibrated shock, hand-to-mouth households suffer consumption-equivalent welfare losses of −4.1%, nearly 60% larger than high-liquid households' −2.6%, with a distributional gradient of −1.5pp. This gradient is convex in shock size: it is approximately five times the average-recession value, suggesting strong non-linearities in the distributional costs of labor market scarring. An empirically scaled training subsidy (peak fiscal cost ~3.6% of steady-state output at the worst quarter) nearly eliminates the distributional gradient at Great Recession severity.

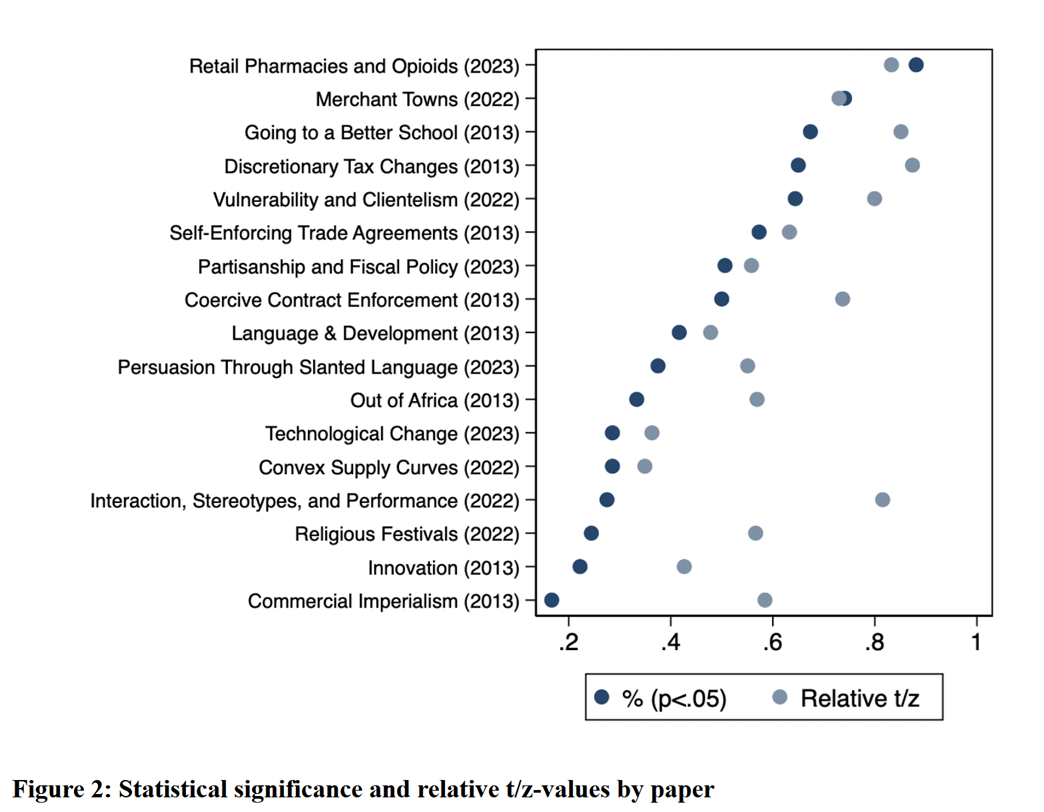

The Robustness Reproducibility of the American Economic Review

We estimate the robustness reproducibility of key results from 17 non-experimental AER papers published in 2013 (8 papers) and 2022/23 (9 papers). We find that many of the results are not robust, with no improvement over time. The fraction of significant robustness tests (p<0.05) varies between 17% and 88% across the papers with a mean of 46%. The mean relative t/z-value of the robustness tests varies between 35% and 87% with a mean of 63%, suggesting selective reporting of analytical specifications that exaggerate statistical significance. A sample of economists (n=359) overestimates robustness reproducibility, but predictions are correlated with observed reproducibility.

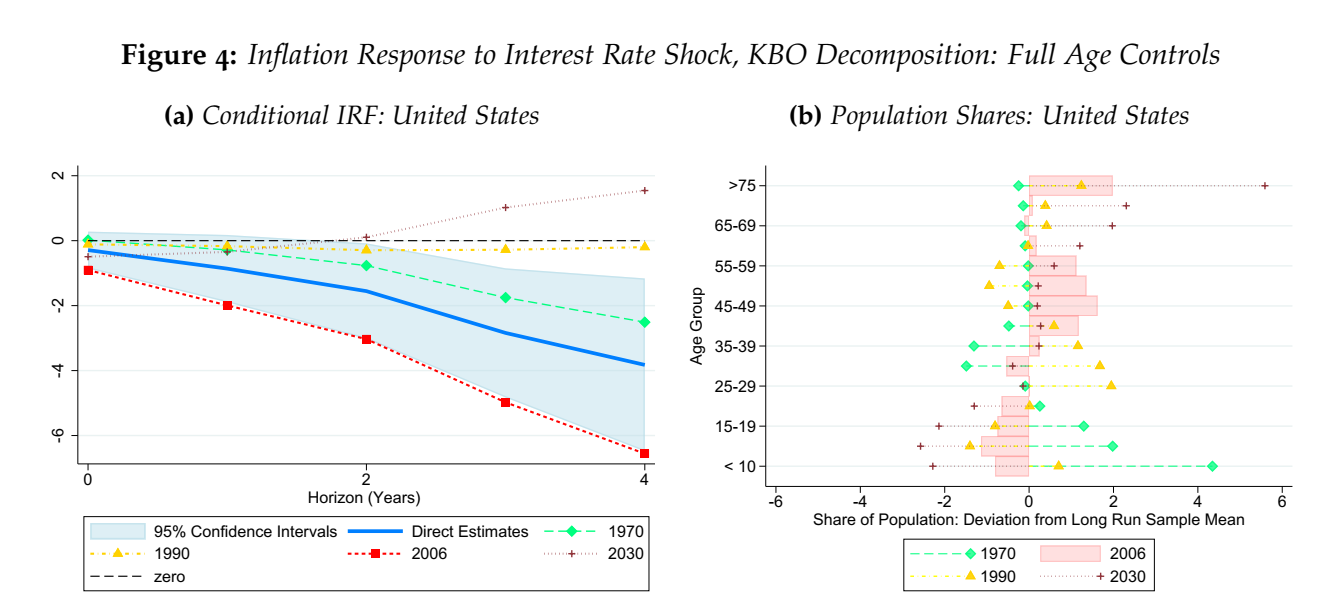

Monetary Policy Goes Boomer: The Effect of Population Age Structure on Policy Transmission

How does the population age structure affect monetary policy? With advanced economies experiencing increased inflation pressures and sluggish growth, it is more important than ever to understand how monetary policy decisions transmit to the macroeconomic variables that policymakers wish to affect. Studying a long-run cross-country panel, we investigate the impact of changing population age structures on the effectiveness of monetary policy transmission to the economy. Monetary policy shocks are identified using a recently proposed trilemma instrument for quasi-exogenous change in policy rates. Our main results are twofold. On the one hand, we provide strong empirical evidence that the intensity of the transmission of interest rate shocks to inflation varies systematically with the age structure of the population: it weakens as the share of young individuals increases, it is less affected by a larger middle-aged population, and declines sharply again as the share of retirees rises. We observe the same pattern for nominal wages and real house prices. On the other hand, demographic structure is found to have more transitory effects on the responsiveness of real aggregate variables such as output, consumption and investment, with older populations delaying the impact of monetary policy. We find no impact on transmission to unemployment.

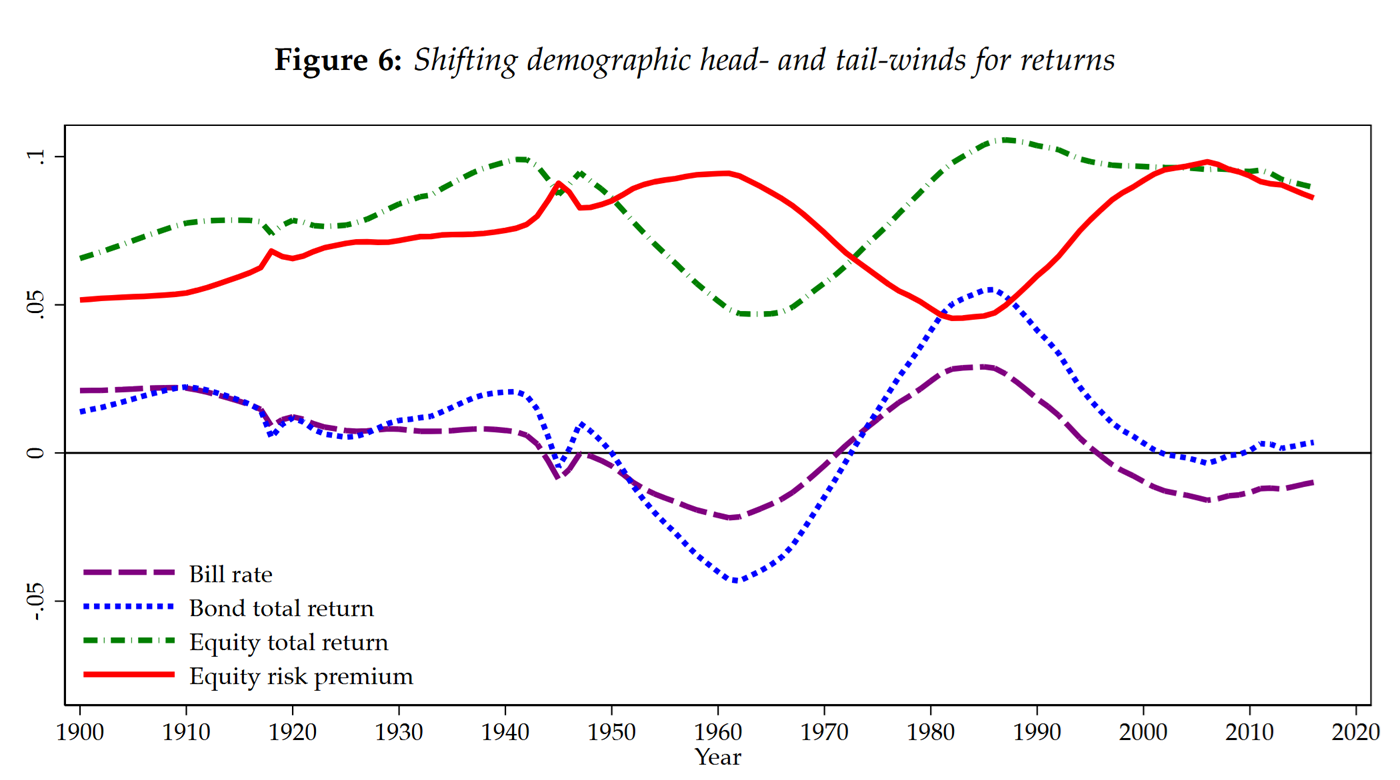

The Savings Glut of the Old: Population Aging, the Risk Premium, and the Murder-Suicide of the Rentier

Population aging has been linked to a global savings glut and a decline in safe real interest rates. Conversely, risky real returns have not fallen as much, if at all, with equity risk premia on the rise. An existing literature can explain changes in safe rates using demographics. We go further to account for divergent returns on different assets as well as the underlying surge in the wealth-income ratio and its asset composition. Empirical evidence from historical panel data shows that demographic shifts are correlated with asset returns and risk premia. We build a heterogeneous agent life-cycle model with two assets (a safe bond and equity) and with aggregate risk. Aging demographics can help to simultaneously explain three key trends: the rising wealth-income ratio, the falling risk free rate, and an increasing risk premium. The shifts exert less pressure on risky returns as high-wealth elderly reallocate away from equities: aging makes retirement saving a "crowded trade" but more so for bonds. Projecting our model to 2050, aging pushes the safe rate below zero, but the risk premium remains elevated, as post-boomer demographics push asset returns to unprecedented and persistently low levels.

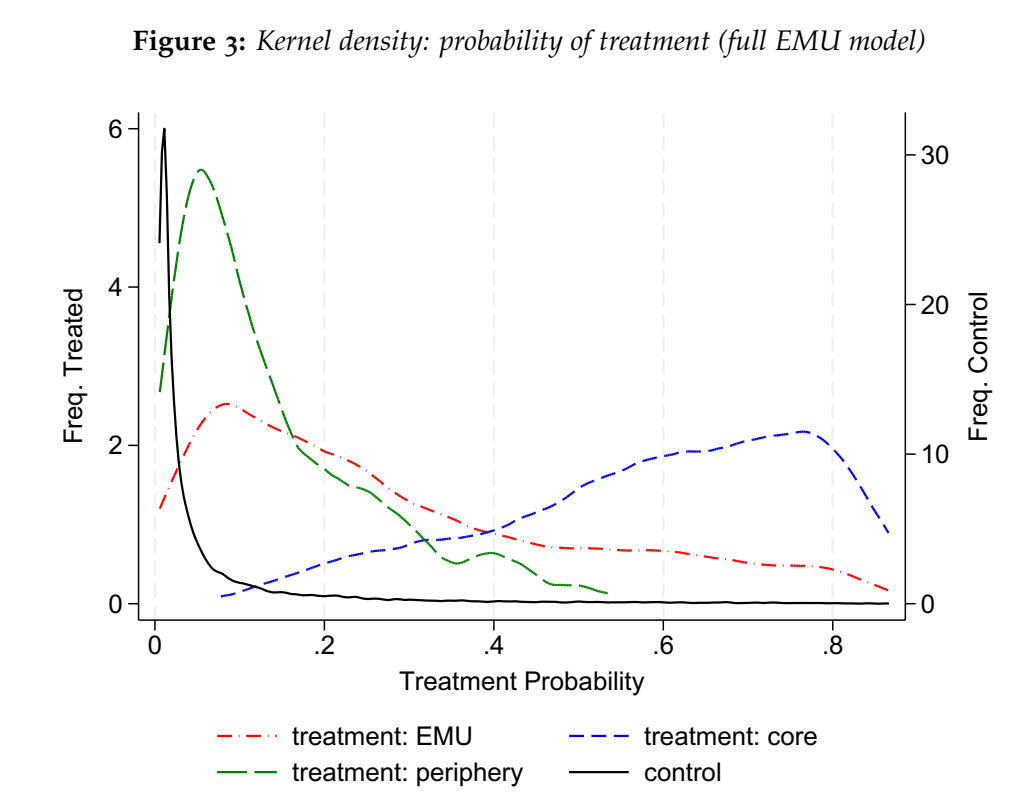

A union divided? The euro and trade in the core and the periphery

Has the euro improved trade evenly across member states? This paper revisits the impact of the euro on trade, focusing on systematic heterogeneity between core and peripheral members. I develop a stylized model linking trade flows to two mechanisms implied by monetary integration: the elimination of bilateral exchange-rate volatility and potential relative price-level convergence upon entry. The model predicts heterogeneous effects depending on structural characteristics of member economies. Using bilateral trade data from 1960-2018, I estimate a gravity model with Poisson pseudo maximum likelihood and apply a doubly robust inverse-propensity score weighting estimator. I find that the average EMU effect masks substantial heterogeneity across member states. On average, euro membership increases trade by about 6%, but trade originating from core members increased by an estimated 12%. Trade between periphery members is estimated to increase by a similar amount, but flows from the periphery to core decline by an estimated 7%, consistent with predictions from the theoretical model.

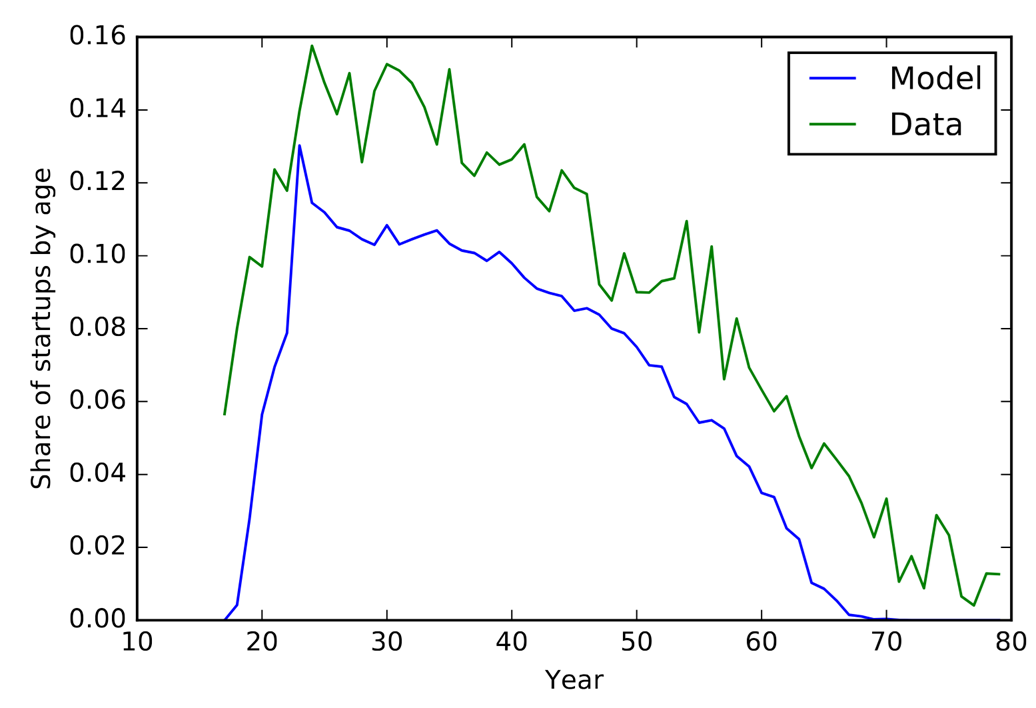

An Aging Dynamo: Demographic Change and the Decline of Entrepreneurial Activity in the United States

The rate of new business startups has fallen drastically over the last thirty-five years, a trend that accelerated after the year 2000. Other measures of business dynamism, such as the job reallocation rate, are consistent with this trend. This has raised serious concern, given the effect that young, high-growth firms have been shown to have on employment, and may also have on innovation and growth. The timing of this decline coincides with the start of a steady increase in both the life expectancy and average age of the workforce. I document that an individual's propensity to select into entrepreneurship follows a 'hump shape' as they age. To account for both individual behavior and aggregate trends, I construct a life cycle model of entrepreneurial choice, studying a number of channels that link demographic forces to entrepreneurial selection. I find that demographic channels can account for a large portion of the recent decline in startup activity. This model predicts that entrepreneurial activity will continue to decline as the pool of potential entrepreneurs continue to age. I conclude with a discussion of the potential policy tools that will affect individual's life cycle risk attitudes and the predicted effects that such measures will have on the rate of new business startups.

Publications

2025

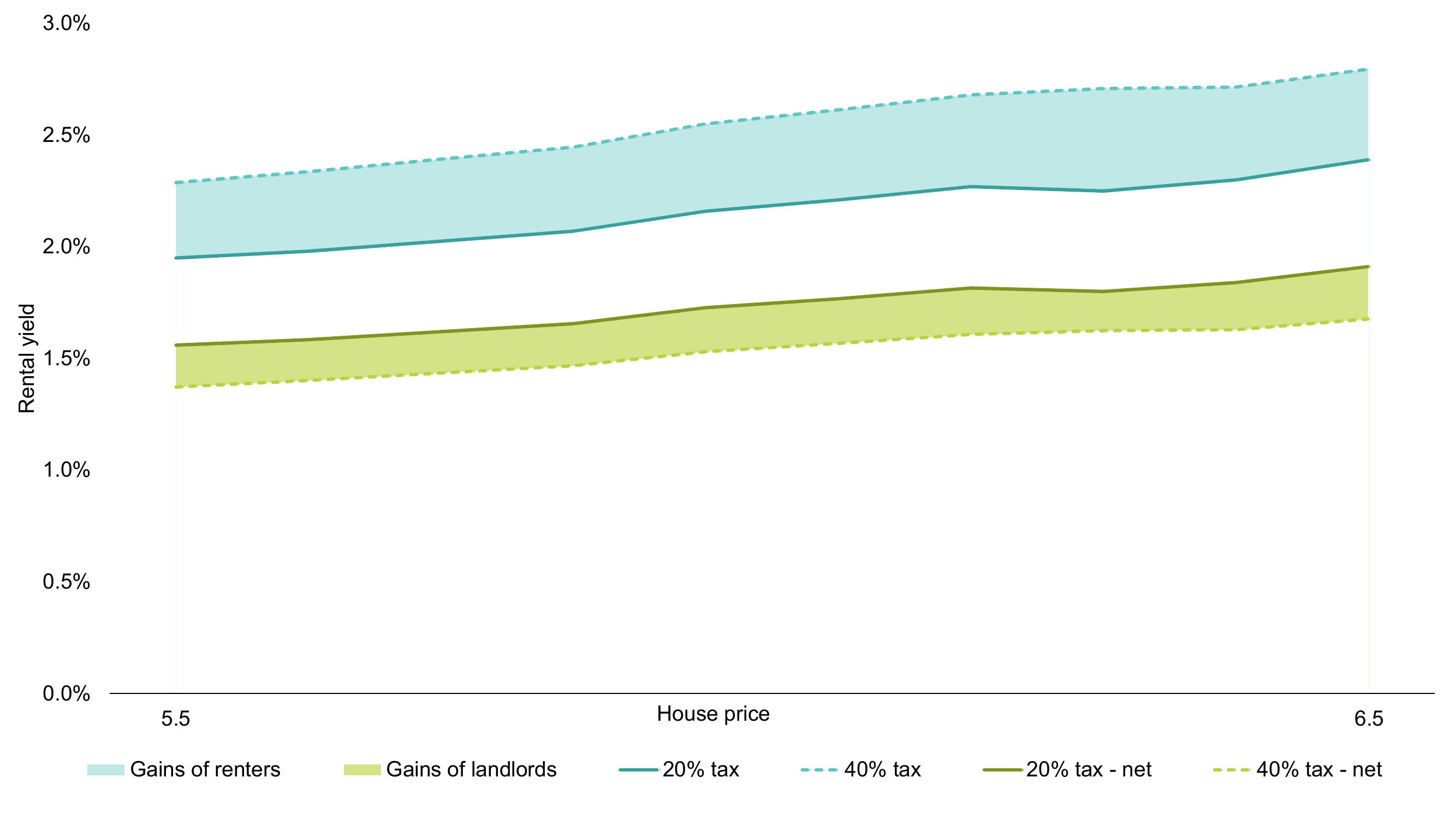

Housing policy, homeownership, and inequality

Policymakers are grappling with widening disparities in income and wealth. For most households, housing assets constitute the largest component of wealth. While housing has been extensively studied in the heterogeneous-agent macroeconomic literature, there is limited guidance on the distributional consequences of housing policy. This paper studies the relative impacts of a range of housing policies on inequality and welfare. We develop and estimate a quantitative life-cycle model in which households endogenously choose between renting and owning, and may become landlords. The model allows us to assess the distributional effects of borrower-based macroprudential limits, institutional investor participation in rental markets, rental income taxation, and housing supply policies. Calibrated to the Irish housing market, the model quantifies policy impacts on homeownership, welfare across the wealth distribution, and broad measures of income, wealth, and consumption inequality. We show that the distributional effects of housing policies depend critically on credit conditions: policies that appear regressive or benign in isolation can have markedly different, and in some cases reversed, effects under tight versus loose credit regimes.

2023

A match made in Maastricht: The average treatment effect of the EMU on trade

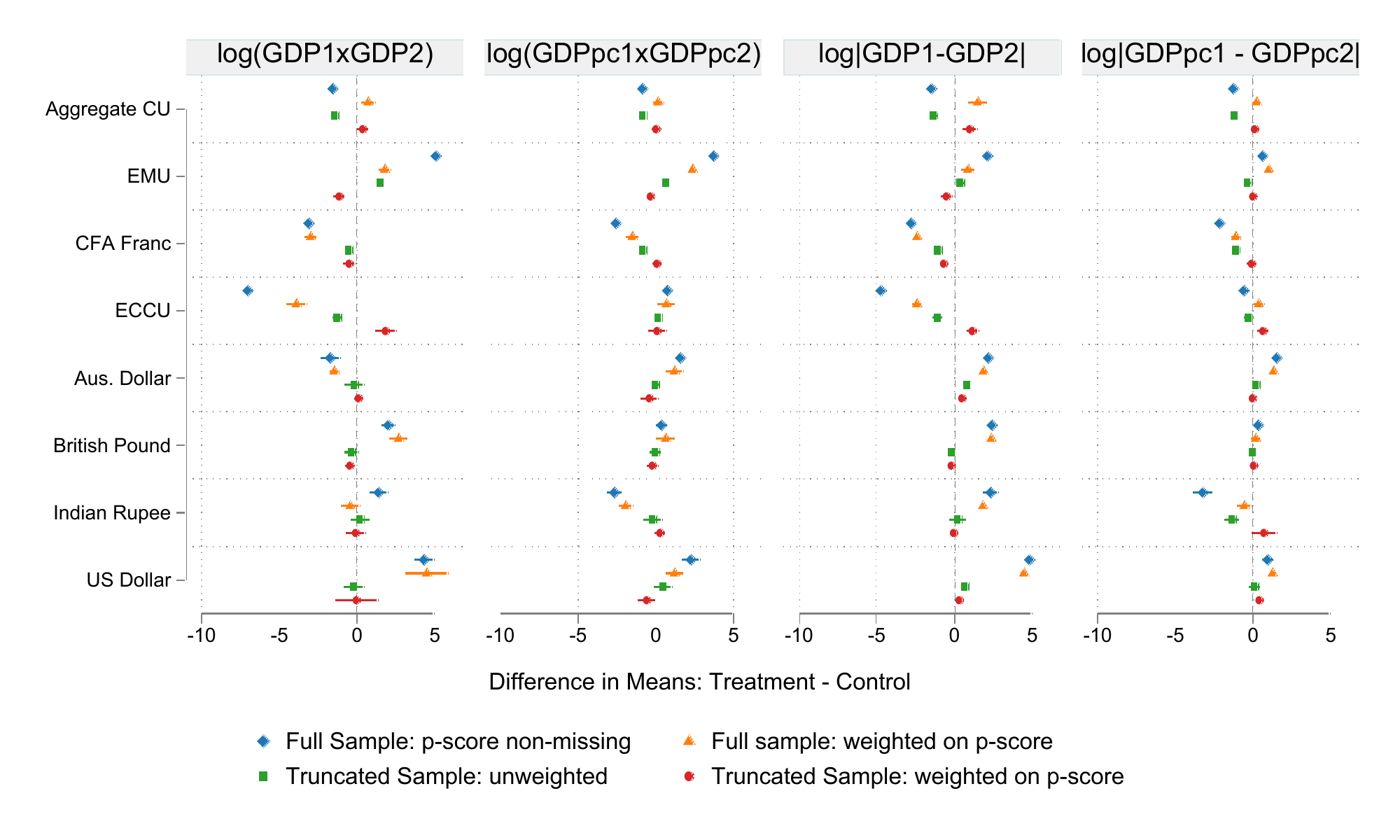

Why do estimates of the European Monetary Union (EMU) effect on trade vary so greatly? Rose (2017) shows that the largest factor determining the size of EMU trade estimates is the choice of sample, with studies using only European or rich countries finding smaller impacts than those using more complete trade datasets. I push this question one step further, asking instead: what is the appropriate comparison group with which to study the euro's trade impact? Using a first stage estimation of selection into the EMU and a robust propensity score weighting estimator, I extend the work of Millimet and Tchernis (2009) to a larger dataset of countries and years, showing that gravity estimates of the euro effect on trade are smaller when sample truncation and weighting brings the differences in observable characteristics between EMU and non-EMU pairs close to zero. Utilizing a Poisson pseudo-maximum likelihood approach, I find that estimates using this more robust estimator reflect the same pattern, but with significantly less initial upward bias. My work suggests that policy analysis in trade should be more careful to consider the comparability of "treated" and "control" observations, and more readily utilize propensity score methods as a data driven approach to rebalancing samples when differences across these groups are large.

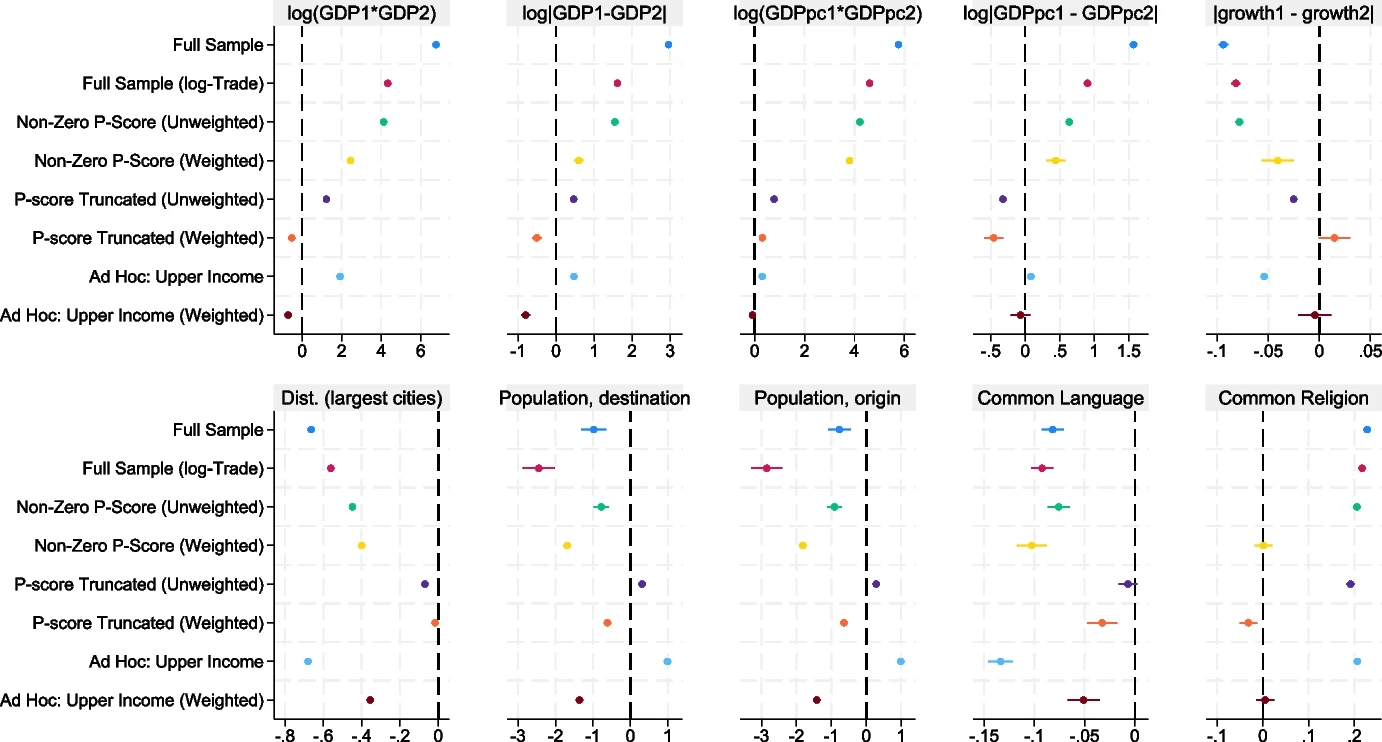

Many unions, one estimate? Disaggregating the currency union effect on trade

A large literature estimates the impact of currency unions on trade. Often ignored in these estimates are the dramatic differences in the characteristics of countries adopting common currencies, hidden by aggregation into a single currency union effect. I show that currency unions have substantial differences in their observable characteristics, relative to non-unions, making them a poor comparison group for estimation of policy treatment. Further, these differences are heterogeneous across individual currency unions, making one aggregate estimate likely inappropriate. Using inverse propensity score methods, I find that adjusting these gravity equation estimates to account these differences, both via weighting and via sample adjustment, meaningfully impacts the estimated policy effects. I find a wide range of currency union effects across individual, disaggregated, currency unions. My results suggest that future work on currency unions, and other macroeconomic policies, should be careful to check for such underlying heterogeneity when estimating policy effects.

Growing older and growing apart? Population age structure and trade

This paper explores the empirical relationship between population age structure and bilateral trade. I include age structure in both log and PPML formulations of the gravity equation of trade. I study relative age effects, using differences in the demographic structure of each country-pair. I find that a relatively larger share of population in working age increases bilateral exports. This is robust to various estimation models, as well as to changes in the method of specifying the demographic controls. Old-age shares have a negative, but less robustly estimated impact on trade. Estimating instead the balance of trade between trading partners produces similar results, with positive effects of age structure peaking later in working life. Global populations are poised to undergo a massive transition. Trade a crucial way that the demographic deficits of one country may be offset by the dividends of another as comparative advantages shift along with the size and strength of their underlying workforce. My work is among the first to quantify the effect of relative age structure between two countries and their bilateral trade flows. Focusing for the on aggregate flows, relative age shares, and PPML estimates of the trade relationship, this paper provides the most comprehensive picture to date on how age structure affects trade.

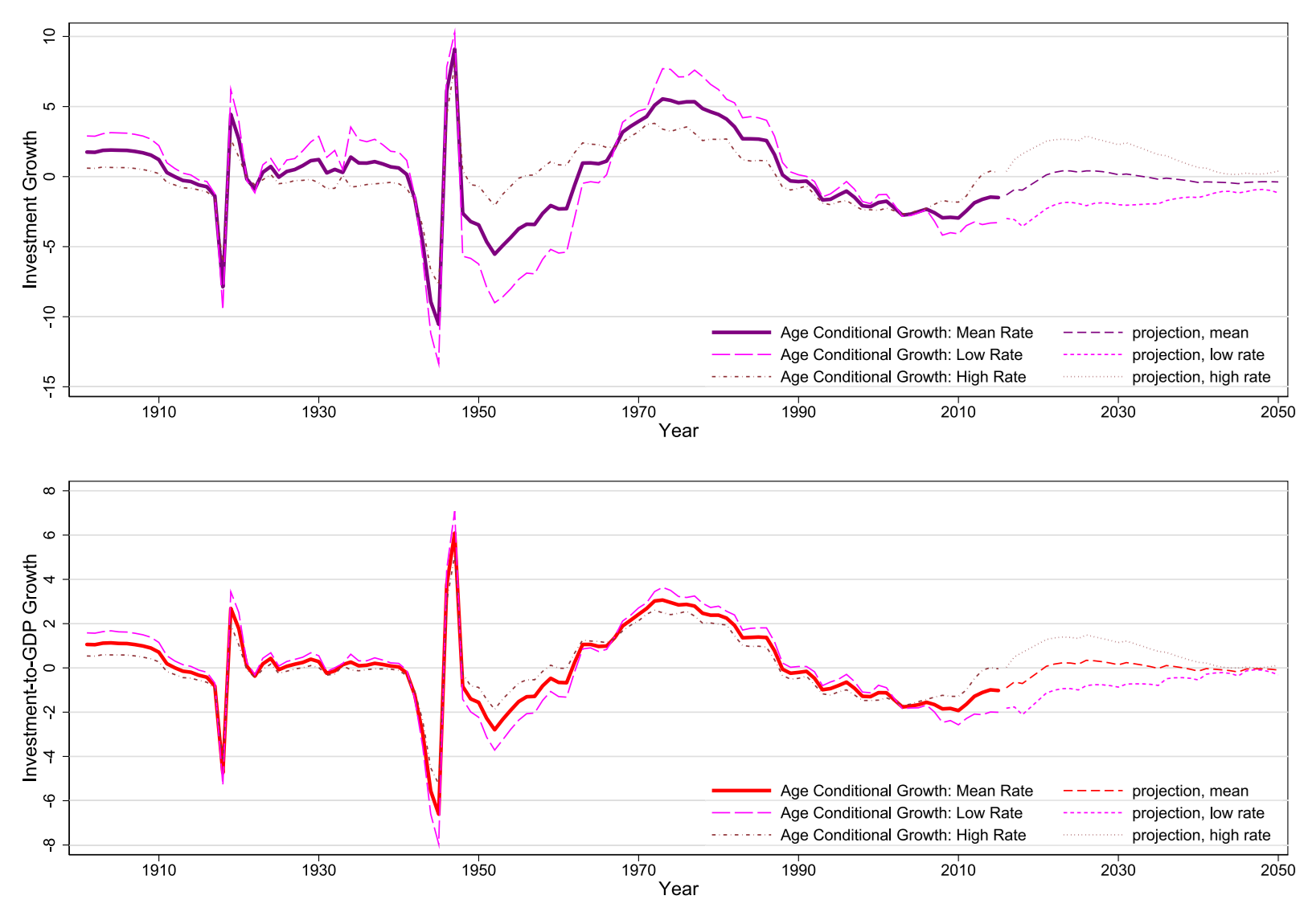

Population age structure and secular stagnation: Evidence from long run data

A large literature has reopened the secular stagnation hypothesis, first proposed near the end of the great depression as a warning for anemic growth resulting from long run trends in population aging. In this paper, I explore the relationship between population age structure and growth in: investment, consumption and output, in a long run panel of advanced economies. The evidence is largely consistent with proposed channels for secular stagnation. Investment growth, in its level and as a fraction of GDP, appears much stronger in young populations, while facing demographic headwinds in older economies. Consumption and output growth are positively associated with late career workers, with a negative relationship coming from both young and old dependents. Consistent with the recent secular stagnation literature, interest rate channels appear to have strong interactions with population age structures. I find that for investment and output growth, estimated impacts of age-structure are more pronounced in low interest rate environments, with high rates mitigating some of their effect.

2022

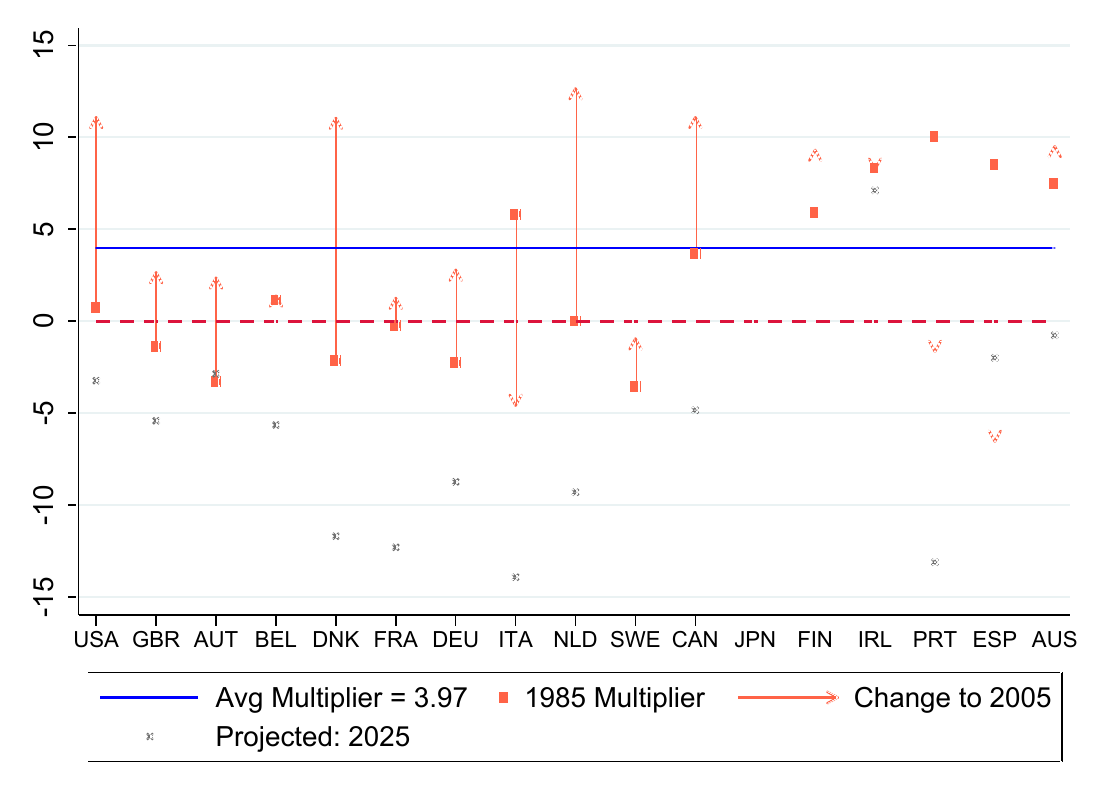

The age for austerity? Population age structure and fiscal consolidation multipliers

Advanced economies face two important trends: population aging and rising debt. In the coming years, it will be critical to understand how policies undertaken by governments interact with their changing age structures. In a panel of advanced economies, I show that fiscal deficit consolidation multipliers are highly sensitive to changes in population age. The demographic transmission of fiscal shocks differs between spending cuts and tax hikes, with important variation within working age and across dependent groups. Tax increases lead to weaker output response in relatively young economies, strengthening as population weights move to middle age, and falling again with large shares of retirees. Output response to spending, on the other hand, shows little change with demographics. The transmission of both policies to fiscal deficits suggests significant age dependence, with important impacts on multipliers when constructed as the ratio of cumulative output and deficit effects. Projecting forward, my estimates expect smaller multipliers as the baby boomer cohort fully retires, with demographics accommodating both tax and spending consolidations in terms of stronger deficit improvements, with tax policy displaying weaker output response.

Okay boomer... Excess money growth, inflation, and population aging

What determines the strength of the relationship between money growth and inflation? A large literature suggests that it has weakened since the 1980s, without a definitive explanation of the cause. I explore how population age structure explains changes in the pass through of money growth rates to inflation. I show that the quantity theory of money holds over long time horizons, with sizable estimates of the impact of money growth on inflation in the short to medium term. Various measures of population age structure have significant impact on the strength of this relationship. These demographics account for an increase in the transmission of money growth to prices in the 1970s and a weakening throughout the great moderation. The baby boomer cohort, now in the age groups around retirement, may exert upward pressure on this money transmission to prices at present, with ambiguous implications in the future as low fertility and rising longevity persist.